Severe Weather Events & Your Business

Courtesy of iii.org

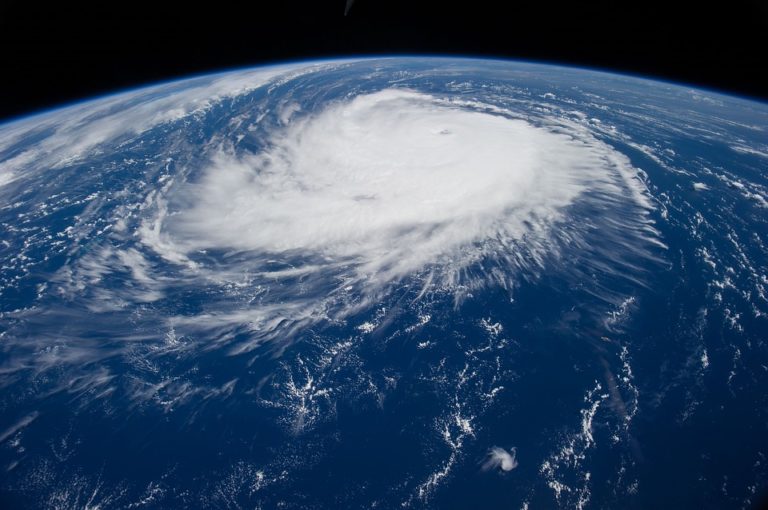

Courtesy of iii.org

With predictions of an above-average hurricane season issued by Colorado State University this week, businesses need to take measures to prepare and increase their chance of surviving, according to the Insurance Information Institute (I.I.I.).

Forty percent of businesses do not reopen after a disaster and another 25 percent fail within one year, according to the Federal Emergency Management Agency (FEMA). But by taking action now to prepare, businesses can increase their chance of getting back on their feet financially and keeping their doors open.

The I.I.I. and the Insurance Institute for Business & Home Safety (IBHS) recommend the following steps:

Develop a Business Continuity Plan

Having a business continuity plan is vital for companies to prepare for, survive and recover from a hurricane. Use IBHS’ free OFB-EZ® (Open for Business) business continuity planning tool to create a plan that focuses on recovering after the initial emergency response. Share your plan with employees, assign responsibilities and offer training so your workforce can collaborate in the recovery of your business. Conduct regular drills to assess and improve response.

Maintain Key Information Offsite

To get your business up and operating as quickly as possible after a disaster, you’ll need to be able to access critical business information. In addition to backing up computer data, keep other critical information offsite such as your insurance policies, banking information and phone numbers of employees, key customers, vendors and suppliers, your insurance professional and others. If you have a back-up site, make sure it’s sufficiently far away so as not to be affected by the same risks that threaten the primary location. Use IBHS’ free EZ-PREPTM severe weather emergency preparedness and response planning toolkit with checklists that can be customized for your company to be sure you have a well-organized plan and are ready to respond when disasters occur.

Create a Business Inventory

Include all business equipment, supplies and merchandise—and don’t forget commercial vehicles.

Review Your Insurance Coverage

The time to review your insurance policy is before disaster strikes and you have to file a claim. It is important that your business have both the right amount and type of insurance for its needs and risk profile. There are two types of policies you can buy as a business owner:

A Business Owner Policy (BOP) is commonly used by small businesses. BOP policies combine property and liability coverage in one policy and are usually less comprehensive than a commercial policy.

A Commercial Multi-peril (CMP) policy combines several coverages—such as commercial property, liability, inland marine and commercial auto—into a single policy. It is typically less expensive to buy a CMP policy than to buy the coverages individually.

Opt for Replacement Cost Coverage

Most commercial property policies provide either replacement cost coverage, actual cash value coverage, or a combination of both. Replacement cost coverage will pay to rebuild or repair property, based on current construction costs. Actual cash value coverage will pay to rebuild or replace the property minus depreciation. Depreciation is a decrease in value due to wear and tear or age. If your business is destroyed and you only have actual cash value coverage, you may not be in a position to completely rebuild.

Consider Tenant Coverage

If you rent or lease a building, consider tenant coverage, which will insure your on-premises property, including machinery, furniture and merchandise. The building owner’s policy will not cover your contents.

Don’t Forget About Flood Insurance

Flooding is not covered by standard commercial insurance policies, so consider buying a separate flood policy. If you’re located in a high- to moderate-risk flood zone, you could be protecting your business from devastating financial loss. Commercial flood coverage is available from the National Flood Insurance Program (NFIP) and provides up to $500,000 in building coverage and $500,000 for contents. You can also get coverage through private insurers.

Visit the Business Insurance section of the I.I.I. website for more information.

RELATED LINKS

Facts and Statistics: Catastrophes

Articles: When Disaster Strikes: Preparation, Response and Recovery; Does My Business Need Flood Insurance?

SOURCES:

Insurance Institute for Business & Home Safety

National Flood Insurance Program